Fees from local traditional banks could be eating away at your money if you receive deposits in a foreign currency on a regular basis. If you’re curious to see if using Wise (formerly Transferwise) can help reduce those fees, then you’re in the right place! (Not familiar with Wise? Be sure to check out this article.) Here I’m going to organize all of the fees and potential fees into a table for easy visual reference. Then I’ll show you my step-by-step process for completing the table using a real world example.

In my example analysis, I’m going to focus on receiving USD as a foreign currency from NihaoPay. However, you could always swap out the NihaoPay information to suit your own needs as you see fit.

Notes Before Getting Started

I decided to make this table for how I would organize the information if I were trying to obtain this information for myself. Of course, all conversion rates and fees are subject to change at any time.

Please note that I’m not a financial expert nor giving financial advice. Everything here is for informational purposes only. My hope is that this may serve as a possible starting point for anyone who may feel overwhelmed with tracking all of the possible fees for accepting deposits of foreign currencies.

Death by a Thousand Paper Cuts

It feel like all of the fees and potential fees are like death by a thousand paper cuts. But have no fear; the info table is here! Now when you look at it in a table format, it doesn’t seem quite as intimidating anymore, right? Well, I hope that’s the case!

| Wise | Traditional Bank | |

|---|---|---|

| Beginning amount | ||

| NihaoPay payout fee | $0.30 USD ACH transfer | $25.00 USD International wire transfer |

| New totals after initial fees | ||

| Fee for receiving USD into a business account | -$0* | |

| Conversion rate from USD to preferred currency | ||

| Conversion fee | ||

| Transfer to traditional bank account (if necessary) | N/A |

It’d be a good idea to double-check that this holds true when doing your own comparison.

I did my best to list the fees in order that they would be encountered. Note that the conversion rate and conversion fee may be a bit tricky to separate out, especially since the conversion fee may vary based on the amount of money you are converting. I wanted to list them separately to make it easier to visually see all of the fees that we need to be looking for when completing the chart.

Keep in mind that the fee for receiving USD may be based on that USD or your local currency, so that could also affect the order for calculating fees.

My biggest piece of advice here is to not worry about getting everything perfect. It’s totally fine if you need to switch rows or even combine them as I’ll do later when working through them. There’s no right or wrong way to organize the information as long as it works for you. As you’ll see, figuring out the fees isn’t an exact science when the conversion rates are constantly changing and traditional banks aren’t always transparent about their fees.

Why Use South Africa for the Example

I decided to use South Africa in my example for a couple reasons. First and foremost, teaching English online to students in China is becoming increasingly popular in South Africa. However, there are often still roadblocks for them being able to accept payments from China using the Chinese payment methods. NihaoPay does work with South Africa, but they don’t support the South African rand (ZAR). Therefore, using USD would be the cheapest option for them to receive payouts from NihaoPay.

I’m also friends with a fellow online English teacher from South Africa who has already been using Wise to accept USD payouts from NihaoPay. He independently determined that despite all of the fees, this method was the best option for him a few years ago. So he’s been able to help answer some of my questions too.

Putting the Chart Into Action

Using the information in the table above, I set out to run a comparison between accepting payouts in USD to Wise or directly to a local bank in South Africa. It was suggested that I use Capitec Bank and First National Bank in my analysis in addition to Wise. I’ll give you a breakdown of my process and conclusions, while using the above table for reference to ensure that I included all possible fees to the best of my ability.

Wise vs. Capitec Bank vs. First National Bank

For this example, let’s pretend that we were expecting a payout of $1,000 USD from NihaoPay. I decided to use this amount for the sake of simplicity and clarity. Of course, we would need to imagine that this is the amount that NihaoPay would be transferring AFTER transaction fees have already occurred. The transaction fees remain the same regardless, and this order is exactly how the process works anyway.

| Wise | Capitec Bank | First National Bank | |

|---|---|---|---|

| Beginning amount | $1,000.00 USD | $1,000.00 USD | $1,000.00 USD |

| NihaoPay payout fee | -$0.30 USD | -$25.00 USD | -$25.00 USD |

| *New totals after initial fees | $999.70 USD | $975.00 USD | $975.00 USD |

For now, we’ll just use the new total row in the following tables since that’s all we need moving forward. I’m doing that to reduce redundancy and to simplify the following tables. I’ll add the first two rows back on the last table, so we can see all of the information together at the end.

Wise

Fortunately, Wise includes a conversion calculator on their website. However, you must pay attention to see if it also includes the transfer fee. Based on my research, it seems that the US based calculator included the bank transfer fee (the fee to move the money from Wise to the local bank) for me, but when my friend in South Africa used their calculator, it only showed the conversion rate, not including the transfer fee (and possibly not the conversion fee either, but that was a bit unclear).

If you are unsure about the fees that are included in the Wise calculator, it’s possible to call or email them. They have been very responsive in my experience, even though their email reply to me ended up in my junk folder.

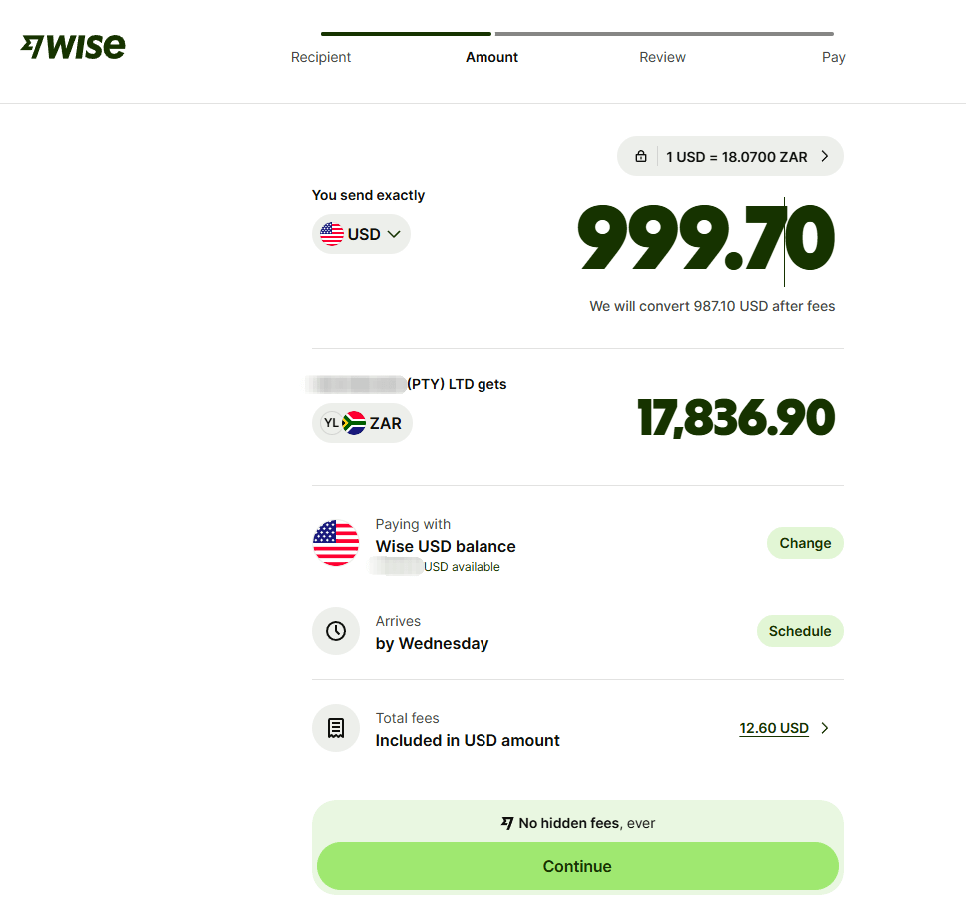

For the sake of today’s experiment though, we’ll just use a screenshot from my friend’s Wise business account since this is the easiest and fastest way to complete this math journey. Plus, this is more accurate than trying to take a guess at the bank transfer fee. The screenshot below shows both a conversion of USD to ZAR and the transfer of said ZAR into his local South African bank account.

In the above screenshot, you can see that the fees for Wise were listed as $12.60 USD, and the conversion rate was 1 USD = 18.0700 ZAR. Wise shows a single amount for both the conversion and transfer fees, so for the sake of completing the table, we’ll just ignore separating out the fees and focus on the final total instead. That’s the most important piece to this puzzle since that was our ultimate goal anyway.

Here’s where we’re at so far:

| Wise | Capitec Bank | First National Bank | |

|---|---|---|---|

| New totals | $999.70 USD | $975.00 USD | $975.00 USD |

| Fee for receiving USD into a business account | -$0 | ||

| Conversion (rate and fee) from USD to preferred currency | See above screenshot from Wise | ||

| Transfer to traditional bank account (if necessary) | See above screenshot from Wise | N/A | N/A |

| Final totals | R17,836.90 |

Capitec and FNB: Conversion Rates and Fees

Yes, I’m going out of order from the chart a bit here, but just you’ll see why when we get to the next part. I tried to put the chart in a logical order, but its primary purpose is to simply organize the information we need, regardless of the order that it’s obtained.

Traditional banks aren’t always as transparent with their conversion rates and fees, so they don’t typically have conversion calculators on their websites. Therefore, I decided to just use Google’s conversion rate on the same day that my friend’s Wise screenshot was taken. This isn’t a perfect option, but it should give us a rough idea of what a traditional bank’s conversion rate could be. In fact, Google’s conversion rate on this date was 1 USD = 18.0754 ZAR, which was better than Wise’s at 1 USD = 18.0700 ZAR, for a difference of Google converting 0.0054 more ZAR per US dollar.

One could make the argument that perhaps it would be more fair to use the same conversion rate as Wise (without the fees) to calculate this. However, this article explained that because Wise specializes in currency conversions and doesn’t have all of the bells and whistles of a traditional bank, they’re often able to offer better conversion rates and lower fees. Therefore, by using Google’s conversion rate instead of Wise’s, I’m actually giving the traditional banks an unlikely advantage.

Updated chart (we’re almost done!):

| Wise | Capitec Bank | First National Bank | |

|---|---|---|---|

| New totals | $999.70 USD | $975.00 USD | $975.00 USD |

| Fee for receiving USD into a business account | -$0 | ||

| Conversion (rate and fee) from USD to preferred currency | See above screenshot from Wise | R17,623.52 (Google estimate) | R17,623.52 (Google estimate) |

| Transfer to traditional bank account (if necessary) | See above screenshot from Wise | N/A | N/A |

| Final totals | R17,836.90 |

Capitec & FNB: Fees for Accepting Foreign Currency

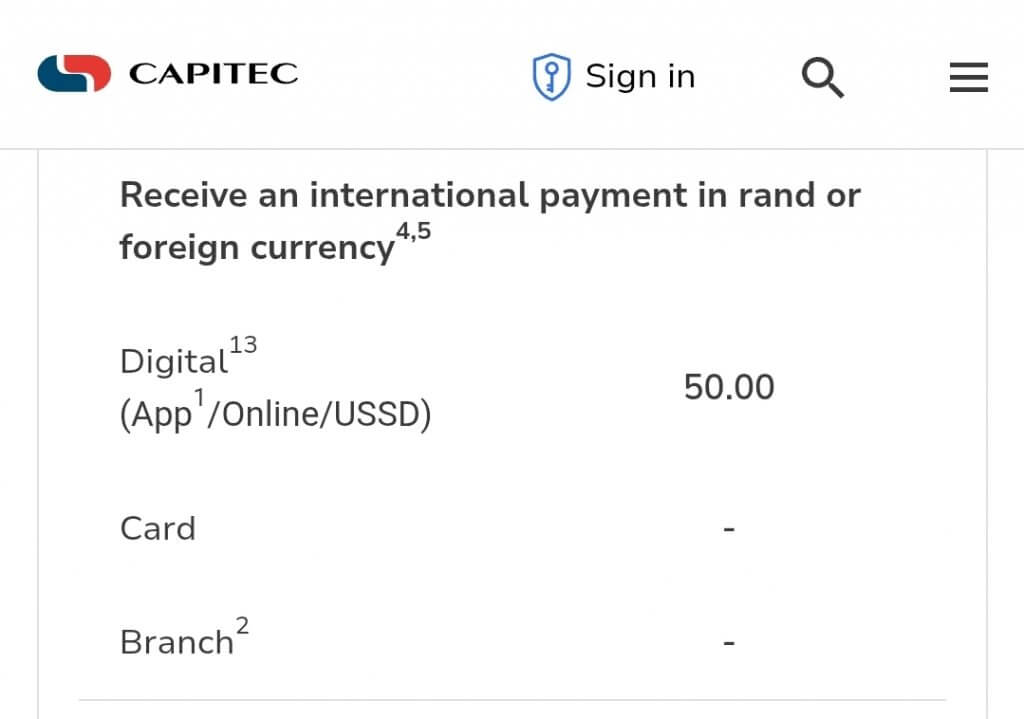

I was able to find that Capitec charges a flat rate fee of R50.00 for receiving a foreign currency, regardless of the amount received. Easy peasy!

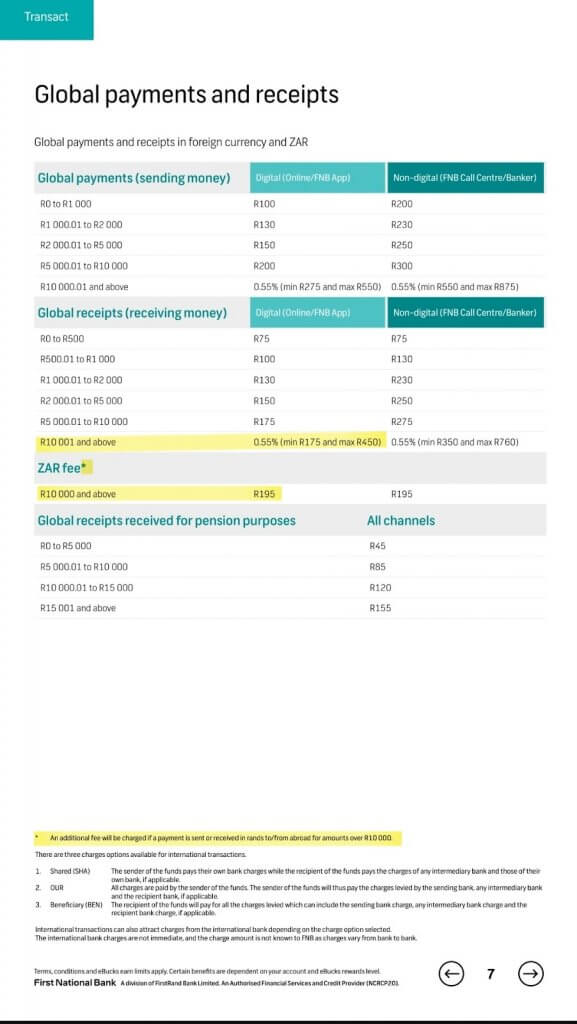

First National Bank doesn’t have a flat rate fee for accepting foreign currency. Instead they adjust their fees based on the amount being received. They also add on an additional fee for large transfers, as you can see in the highlighted areas on the screenshot below.

We already know that the transfer amount will be over R10,000, so now we are subject to both fees in this example.

Under “Global Receipts” the fee for the amount we need transferred is 0.55% or at least a minimum of R175. So let’s take our converted amount of R17,623.52 and multiply that by 0.55%. We end up with R96.93. Since that’s below the minimum fee amount of R175, we’ll use the minimum fee amount of R175, although we should keep in mind that the actual fee could possibly be higher.

Don’t forget to include that secondary flat rate fee of R195!

Now we can plug in those final fees and subtract them from our Google estimated conversions:

| Wise | Capitec Bank | First National Bank | |

|---|---|---|---|

| New totals | $999.70 USD | $975.00 USD | $975.00 USD |

| Fee for receiving USD into a business account | -$0 | -R50 | -R175* -R195 |

| Conversion (rate and fee) from USD to preferred currency | See above screenshot from Wise | R17,623.52 (Google estimate) | R17,623.52 (Google estimate) |

| Transfer to traditional bank account (if necessary) | See above screenshot from Wise | N/A | N/A |

| Final totals | R17,836.90 | R17,673.52 | R17,253.52 |

Let’s Discuss the Results!

At a glance, we can see that using Wise to accept payouts in USD from NihaoPay was the clear winner compared to local traditional banks in South Africa in this specific example. Wise saved R163.38 compared to Capitec and R583.38 compared to First National Bank. According to Google’s conversion rate as cited above, that’s $9.04 USD and $32.27 USD respectively.

Keep in mind that I’d also given the banks the benefit of the doubt. I used an unlikely better conversion rate and used the bare minimum fee rate for First National Bank. This way I really put Wise to the test against traditional banks since the savings are likely higher than what I calculated here.

Something worth noting is that the conversion and bank transfer fee from Wise was shown to be $12.60 USD or R227.68 according to Wise’s conversion rate. When we consider it from this perspective, maybe Wise isn’t the clearest winner in terms of fees. However, what seemed to be the determining factor here was using Wise to eliminate nearly all of that hefty $25 USD international wire transfer fee from NihaoPay. If that international wire transfer fee hadn’t been so high to begin with, Wise may not have come out as a clear winner for cost savings in this specific example.

A Note About Conversion Dates

A traditional bank is likely to convert any received foreign currency to the local currency on the day the money is received. However, Wise will hold the funds in the currency in which it was received. Then you have the choice to manually convert funds as needed or you could set up an auto conversion. Wise can trigger an auto conversion based on the parameters you set. If you’re able to wait, an auto conversion is another way that Wise could make your funds go further.

Does That Mean I Should I Use Wise?

Like I said before, I’m not going to give you financial advice, and besides, everyone’s situation is unique! What I can tell you are some things you may want to think about when considering using Wise:

- Do you travel internationally or have other international monetary needs?

- Maybe you’ll find Wise useful in more ways than one.

- Does Wise offer a debit card in your country?

- If so, maybe you don’t need to worry so much about transferring funds from Wise to a local traditional bank.

- Which do you value more: savings or convenience?

- Even if Wise would potentially save you money, it would still mean additional effort on your part to move money from that account to your local bank on a regular basis. Maybe you’re totally fine jumping on their app or site to transfer funds regularly, or maybe you feel overwhelmed with adding another task to your to-do list. It’s totally fine if you think that eliminating that extra task is worth the cost of the potential savings.

- You can always change your mind!

- Regardless of which option you choose initially, you can always change your mind and switch which account you’d like NihaoPay to send your payouts to. For this, you would need to contact me or NihaoPay directly to get a bank account change form.

Do what you think would best suit you for your current situation, and move forward with that decision with confidence! If your situation changes, you don’t need to feel stuck because you can always make changes later as needed.

Hopefully, seeing how you can organize all of the potential fees into a table and working through how to complete it has helped reduce any anxiety and made wrapping your head around all of the information less confusing!

Want to Use Wise to Accept Payouts from NihaoPay?

Use your Wise business account information when asked for your bank account details in the NihaoPay Merchant Application. Just make sure to list Wise’s US address!

Already use NihaoPay and want to change where they send your payouts? Reach out to your NihaoPay contact about it. If I’m your NihaoPay contact, you can send me an email directly.